Listen to a podcast-style summary of this blog post

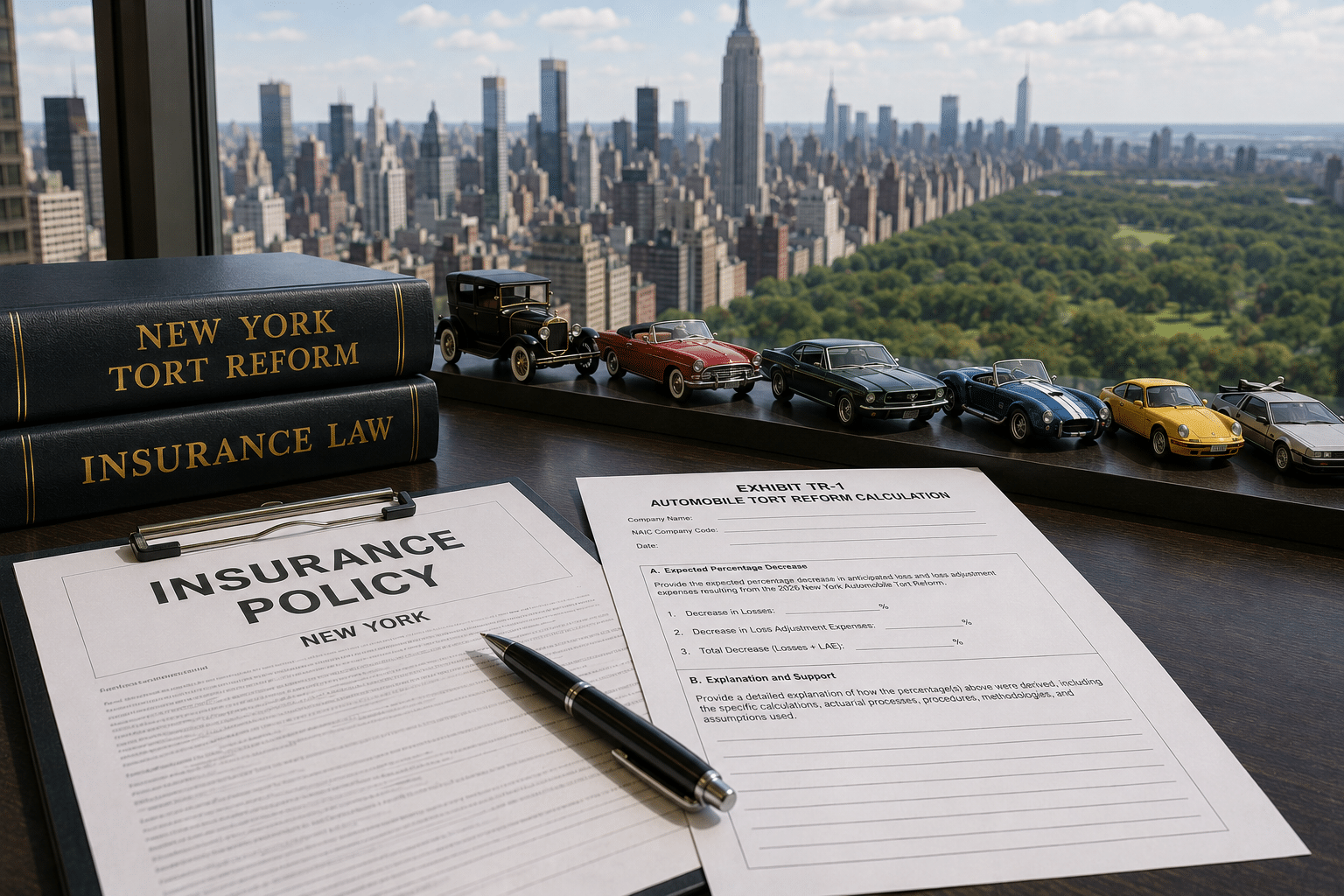

New York’s 2026 automobile tort reform introduces new filing requirements that will affect every insurer writing motor vehicle insurance in the state. On July 1, 2026, the New York Department of Financial Services (“DFS”) issued Circular Letter No. 3 summarizing the law changes affecting motor vehicle insurance that were enacted to address factors contributing to rising premiums. The legislation includes reforms aimed at reducing fraudulent and abusive claim practices, limiting certain non-economic damage recoveries, and modifying New York’s personal auto rate filing requirements. Any insurer writing automobile insurance in the state will need to comply with the new filing requirements in pending and future filings.

In this blog, we’ll walk you through what has changed, what this means for auto insurers, and how Perr&Knight can assist.

What Changed?

The 2026 reforms fall into three primary categories: changes to the Fraudulent Insurance Act, revisions to New York’s serious injury and non-economic damages provisions, and modifications to flex rating for nonbusiness motor vehicle insurance. While each change has regulatory significance, its expected impact on insurers varies considerably.

First, the reforms expand the definition of a fraudulent insurance act to include individuals who hire, encourage, or orchestrate staged motor vehicle accidents. The intent is to strengthen prosecution of organized insurance fraud and deter staged accidents. Although the impact is uncertain, the change is expected to reduce fraudulent claims over time.

Second, the reforms address non-economic losses and remove the “90/180-day” serious injury category, which previously allowed certain non-permanent injuries that substantially disrupted an injured person’s daily activities to qualify as serious injuries. This change is expected to reduce the number of claims eligible for non-economic damages.

The order in which fault and serious injury are evaluated has changed. Previously, there was no sequence for determining fault and serious injury; now the reform requires fault to be established first. By resolving fault before evaluating serious injury, the reforms may reduce unnecessary litigation and defense costs in cases where liability cannot be established.

The reforms also impose a $100,000 cap on non-economic damages for certain claimants engaged in specified wrongful conduct, such as operating an uninsured vehicle, driving while impaired, or committing a felony at the time of the accident. In addition, New York has adopted a modified comparative negligence standard, which is expected to eliminate recovery for personal injury claimants who are found to be more at fault than the insured against whom recovery is sought.

Third, starting November 27, 2026, the state will eliminate the ability of personal auto insurers to implement rate increases of up to 5% without prior approval. Insurers may decrease rates by up to 5% without prior approval until May 27, 2030.

While the legal reforms vary in scope, collectively they are expected to reduce claim frequency, claim severity, and loss adjustment expenses. This leads us directly to the DFS’s new filing requirements discussed below.

What Does This Mean for Insurers?

Any insurer with a pending New York motor vehicle rate filing, or planning to submit a future motor vehicle filing, is affected by the new requirements. Pending filings must be updated by August 31, 2026. The DFS expects insurers to evaluate the impact on claim frequency, claim severity, loss adjustment expenses, and any other relevant factors. Insurers must consider the impact of the reforms and provide supporting information in the new Exhibit TR-1, Automobile Tort Reform Calculation. Exhibit TR-1 requires insurers to identify the expected percentage decrease in anticipated loss and loss adjustment expenses resulting from the reforms. It also requires a detailed explanation of how that percentage was derived, including the specific calculations, actuarial processes, procedures, methodologies, and assumptions used.

How Can Insurers Estimate the Impact?

When a reform is passed, insurers may have little or no post-reform loss experience but still need to incorporate the reform’s impact in their program. How does an insurer estimate the impact without credible post-reform data? Historical experience, auto industry knowledge, and claim metric benchmarks can all inform the estimate.

Whatever the approach, the estimate needs to have actuarial support to ensure a reasonable impact on the company’s book of business.

How Perr&Knight Can Help

Navigating New York’s tort reform and the resulting filing requirements can be challenging. Perr&Knight offers a strong team of actuarial consultants with extensive New York filing experience and knowledge of the reform to help insurers navigate these new requirements with confidence.

Perr&Knight has published the Q4 2025 edition of State Filings Pulse, highlighting the latest trends in approval times, rate changes, and key filing developments across states.

California and New York Converge as the Slowest States for Homeowners Rate Approvals

In 2025, the median time to approval for homeowners rate filings in New York increased sharply to 273 days, up from 121 days in 2024. This brings New York nearly in line with California, which continues to have the longest approval timelines at 283 days.

While California has historically been the slowest state, New York’s increase in 2025 reflects a shift toward a more rigorous and iterative regulatory review process. Approval times in New York rose steadily through the first three quarters of the year, peaking at over 300 days in Q3 before declining in Q4. However, this late-year improvement may not be indicative of future expectations, given it reflects only one quarter and contrasts with the prior trend.

California Approval Timelines for Homeowners Show Signs of Improvement

Despite remaining the slowest state overall, California showed measurable improvement in 2025. Median approval times for homeowners rate filings declined from 340 days in 2024 to 283 days in 2025, with a significant reduction to approximately 200 days in the second half of the year.

In addition, 2025 saw the approval of the first homeowners rate filings incorporating catastrophe modeling and recognition of the net cost of reinsurance (NCOR). These filings reflect regulatory changes introduced as part of the California Department of Insurance’s Sustainable Insurance Strategy (SIS), which allow the use of catastrophe modeling and NCOR, provided insurers commit to writing in “distressed areas” as defined by CCR § 2644.4.8. This option only became available in mid-2025, making these approvals a notable milestone.

Company

Time to Approval (Days)

Approval Date

Approved Rate Change

California Auto (“Mercury”)

125

12/18/2025

6.90%

CSAA

114

12/18/2025

6.99%

The approval of homeowners rate filings incorporating catastrophe modeling and NCOR, together with reduced approval timelines, represents an encouraging development in California.

Approved Rate Changes Moderate but Remain Elevated

After several years of elevated increases, approved rate changes began to moderate in 2025 across most states. The median approved rate change across all filings declined to 6.5% in 2025, down from 9.3% in 2024. The table below provides details by year and line of business groupings.

Line of Business Grouping

Calendar Year

2021

2022

2023

2024

2025

Homeowners

4.4%

6.8%

10.0%

11.0%

6.6%

Personal Auto

1.7%

7.0%

9.8%

7.8%

2.0%

Commercial & Other Personal

4.5%

5.0%

7.2%

9.1%

7.9%

All Rate Filings

4.0%

5.9%

8.7%

9.3%

6.5%

Despite this moderation, homeowners rate changes remain elevated in highly regulated states. California recorded the highest median approved homeowners rate change at 14.4%, followed by New York at 9.9%.

The higher rate levels in California are closely tied to its longer approval timelines and more restrictive filing environment. Insurers tend to file less frequently and seek larger increases when they do file, resulting in higher approved changes relative to other states. While California is the largest state in terms of premium volume, it ranks twelfth lowest in the number of rate filings approved.

Overall, the data suggests that while rate momentum is slowing nationally, states with longer and more complex approval processes continue to experience higher approved rate changes.

Time to Approval/Disposition by State

The tables below provide a breakdown, by state, of median time to approval/disposition based for the 12-month period ending December 31, 2025.

Rate Filings1,2

Approval Time Range (Days)

Homeowners

Personal Auto

Commercial & Other Personal

0 to 303

AL, AR, AZ, ID, IL, IN, KY, LA, MI, MN, MS, MT, NC, NE, NM, OK, OR, SD, TN, UT, WI, WV, WY

AL, AR, AZ, ID, IL, IN, KS, KY, LA, MN, MS, MT, NC, NE, NM, OH, OK, OR, SD, TN, UT, WI, WV, WY

As we launch this newsletter, it’s worth addressing a practical question many insurance organizations are actively considering: Should we build, buy, or rethink our current approach to regulatory compliance operations?

For many carriers, fronting companies, MGAs, and program managers, the default answer has historically been some combination of homegrown systems, state platforms like SERFF, bureau-generated materials and guidance, and single-purpose tools layered together over time. Historically, that approach worked reasonably well. But as organizations grow, expand into new states, and increase product complexity, the limitations become more apparent.

Homegrown systems, while tailored and often built with current technology, come with an ongoing burden. They require continuous internal investment, compete with other IT priorities, and depend heavily on a limited number of individuals who understand how they work. Enhancements are slow, regulatory updates require constant attention, and over time, the system becomes harder, not easier, to improve and scale.

Single-purpose tools offer a different tradeoff. They can improve a specific step in the process, but they rarely solve the broader problem. Instead, they introduce additional handoffs, often require duplicate data, and create new integration challenges. What begins as an efficiency gain in one area frequently creates inefficiency somewhere else.

Even when these approaches are combined, the result is typically the same: fragmented workflows, inconsistent data, and heavy reliance on manual coordination to fill gaps—especially around communication among stakeholders. That may be manageable at smaller scale, but it becomes a constraint on growth and a source of operational risk over time.

Licensing a platform like PK1Cloud represents a fundamentally different approach.

Rather than each organization building and maintaining its own environment, PK1Cloud centralizes that effort. Development, enhancements, bug fixes, and regulatory updates are handled once and delivered across the platform. This not only reduces cost, but ensures that the system is continuously improving and staying current with changing requirements.

At the same time, PK1Cloud is designed as an integrated operating platform, not a collection of tools. It brings together secure, centralized data, standardized workflows (which can be tailored to fit each organization’s needs), automated communication, broad integrations, and guardrailed AI within a single environment. The result is greater consistency, better visibility, less enterprise risk, and the ability to scale operations without a corresponding increase in complexity.

From a strategic standpoint, the decision is less about technology and more about focus. Organizations that choose to build and maintain their own systems are, in effect, taking on a software development business alongside their core insurance operations. Those that adopt a platform approach can redirect that time, capital, and talent toward core operational initiatives.

That is ultimately the value proposition of PK1Cloud: a more efficient, scalable, and durable way to operate in an increasingly complex environment.

Read on for a closer look at how PK1Cloud delivers these capabilities in practice.

Tim Perr, Chief Executive Officer

PK1Cloud Is Now Live.

Did you know that Perr&Knight has launched PK1Cloud, a unified operating platform designed to modernize and streamline Property & Casualty insurance operations?

PK1Cloud brings together analytics, product design, and compliance within a single, integrated environment. Built on Perr&Knight’s 30+ years of industry expertise, the platform is purpose designed to address the operational and regulatory complexity faced by insurers, program managers, and alternative risk finance organizations.

At its foundation, PK1Cloud aligns three critical dimensions of P&C operations: process, data, and communication.

From a process standpoint, PK1Cloud replaces fragmented, manual workflows with standardized, automated, AI-enabled applications. This reduces operational risk, removes single points of dependency, and improves consistency and control across the organization.

From a data perspective, PK1Cloud establishes a secure, enterprise-wide single source of truth. Built in versioning, validation, visualization, and integration capabilities ensure decisionmakers are working from accurate, trusted information—supporting transparency, scalability, and auditability.

Equally important, PK1Cloud enables more effective collaboration. Intelligent workflows and calendar-aware automation help teams manage dependencies, meet regulatory deadlines, and maintain alignment across stakeholders and functions.

Lastly, we are always adding to and improving the platform; PK1Cloud is designed for long-term evolution. The roadmap for 2026 includes an expanded forms library and the continued rollout of secure, purpose-built AI enhancing insight and decision-making while protecting client confidentiality and data integrity.

The objective is straightforward: to help organizations operate faster, with greater accuracy and confidence. PK1Cloud is a scalable foundation for continuous improvement and sustainable operational excellence in modern P&C insurance.

We invite you to explore PK1Cloud on our website to learn how we are redefining insurance operations.

Bob Cericola, Director, PK1Cloud

StateFilings.com Is Now PK1Cloud Filings.

Did you know that StateFilings.com is now PK1Cloud Filings and is now an integral part of the broader PK1Cloud software ecosystem?

PK1Cloud Filings continues to deliver the structured regulatory workflow capabilities clients rely upon, and is now aligned with Perr&Knight’s vision for coordinating regulatory work across the enterprise.

At its foundation, PK1Cloud Filings is built around a project-based structure that strengthens accountability and execution. Rather than managing filings in isolation, teams organize work into countrywide initiatives and monitor state-by-state progress from a centralized view. Defined process ownership, automated reminders, and centralized project tracking reduce regulatory risk and create more predictable execution across jurisdictions.

The platform also improves visibility across the organization. Real-time status updates, dashboards, reporting tools, and notifications allow actuarial, product, compliance, and leadership teams to track regulatory progress without relying on manual updates or disconnected tracking methods. This shared visibility improves coordination and decision making.

Looking ahead, PK1Cloud Filings will further integrate with other PK1Cloud applications, strengthening the connection between product development, actuarial work, and regulatory filings. This integration will streamline the transfer of product content such as forms, rates, and rules into the filings workflow within a fully auditable system. PK1Cloud Filings will also continue expanding secure AI capabilities designed to protect client data while improving efficiency and accuracy.

The transition to PK1Cloud Filings reflects Perr&Knight’s continued investment in modern regulatory operations, enabling organizations to move from tracking filings to managing regulatory execution at scale.

Did you know that PK1Cloud includes an application designed to help insurers develop and manage their products? Introducing PK1Cloud Product.

Rather than relying on disconnected spreadsheets, document repositories, and manual tracking, Product brings forms, rates, rules, and regulatory intelligence together within one unified platform. The result is a more structured, collaborative, and transparent approach to product development.

PK1Cloud Product supports the entire insurance product lifecycle — from drafting and redlining to review, approval, and finalization. Teams work within a centralized, controlled workspace featuring version management, audit trails, and streamlined workflows. Regulatory insight is embedded directly into the drafting and review process, helping improve accuracy, reduce rework, and strengthen alignment across product, legal, compliance, and filings teams.

Product will continue to expand in 2026. Our roadmap includes access to state-specific checklists, transmittals, and required supporting documentation, enabling teams to prepare and manage filing materials in one place. Advanced comparison tools will allow users to evaluate differences in language, structure, and regulatory requirements across versions and jurisdictions. Secure AI-powered drafting, compliance checks, and intelligent document comparison will further enhance speed, precision, and insight.

PK1Cloud Product reflects our commitment to building a connected ecosystem designed to make insurance product development faster, more consistent, and more confident.

Bob Cericola, Director, PK1Cloud

PK1Cloud Has Reporting Built for the Real World.

Did you know that PK1Cloud Reporting is a powerful application designed to handle the complexity of statistical reporting?

PK1Cloud Reporting delivers reliable, compliant, bureau-ready results and is built specifically to manage the messy realities of client data while transforming it into clean, regulated data extracts. The platform ingests clients’ raw source data in multiple formats and sources and then aligns it to the specific requirements of each bureau and data collection organization. Whether it’s ISO, AAIS, MACAR, or NCCI, PK1Cloud Reporting is built to support reporting across jurisdictions and organizations with confidence.

When source data changes, updates do not require a development cycle. Teams can adjust core lookup table mappings directly, keeping reporting on track without delay.

For clients who prefer automation, PK1Cloud Reporting can securely pull or push files from a client managed repository, reducing manual steps and improving consistency.

Looking ahead, the 2026 roadmap includes key initiatives designed to reduce costs, increase data accuracy, and further streamline statistical reporting operations.

You can count on PK1Cloud to stay ahead of evolving statistical reporting requirements so your team can focus less on compliance risk and more on delivering value.

Nathan Dumont, Product Owner, PK1Cloud Software

Your Subscription Includes Monthly Customer Success Check-Ins.

Did you know that monthly check-ins with the PK1Cloud Customer Success Team are more than routine status meetings, they’re a dedicated opportunity to ensure you’re getting the most value from your PK1Cloud products while staying ahead of change?

These sessions are structured around your priorities. Time is set aside to answer questions, review top-priority or high-severity Service Desk tickets and align on what matters most to your team in the moment. Rather than reacting after an issue escalates, these conversations help proactively address needs before they become obstacles.

Monthly check-ins also provide early visibility into the PK1Cloud roadmap.

Customer Success Team Reviews offer regular opportunities to provide subscribers with demonstrations of recently released features, as well as share insights into upcoming enhancements and explain how new functionalities can be applied to real-world regulatory workflows. This allows you and your team to prepare for changes, adjust processes in advance, and adopt new features with confidence.

Just as importantly, these meetings create space to review existing processes and workflows. With a broad view of how customers across the industry use PK1Cloud, Customer Success Team Reviews can help identify efficiencies, reduce manual steps, and suggest better ways to accomplish everyday tasks using tools you may already have available. Small workflow improvements (such as view customizations, alert usage, or permission adjustments) often result in meaningful time savings over time.

Customers who participate consistently tend to see faster issue resolution, stronger feature adoption, and smoother regulatory operations.

If you’re not currently taking advantage of monthly check-ins, the Customer Success Team is happy to help get them scheduled and tailored to your needs.

Dana Pagliarulo, Director, PK1Cloud Software

PK1Cloud Is Built Around a Seamless User Experience.

Did you know PK1Cloud brings multiple applications together under one platform, and the user experience is intentionally designed to feel that way? A powerful ecosystem only delivers its full value when the interface is simple, consistent, and easy to navigate. That’s why our “One Experience” philosophy is grounded in thoughtful UI and UX design.

In 2026 we are aligning layouts, navigation structures, and visual elements across every application within PK1Cloud, creating a cohesive design language. Whether you’re working in Filings, Product, or Reporting, the platform looks and feels familiar and connected. Users shouldn’t have to re-learn the system; as they move between services, transitions are designed to feel natural and seamless.

By strengthening visual consistency and simplifying workflows, we reduce cognitive load and make it easier to focus on meaningful work. Clear dashboards, predictable navigation, and standardized interactions help teams move faster and operate with greater confidence.

Every update now moves in the same direction, toward a clearer and more cohesive experience across PK1Cloud.

This workflow reflects our commitment to building a unified system — one designed not only to support your work, but to make it more efficient and enjoyable.

Listen to a podcast-style summary of this blog post

Introduction: The Coming Transformation of Rate Filings

For too long, the rate filing process has depended on people rather than systems. Every insurer has lived with some version of the same problem: a small group of analysts and actuaries who “know how it’s done,” spreadsheets scattered across shared drives, and institutional knowledge that travels with employees when they change roles or leave. The result is fragility with single-point dependency risk and a chronic lack of a single source of truth for filings data, documentation, and workflow history.

Even with the introduction of insurance state filings software like SERFF in the early 2000s and its upcoming “modernization,” this issue remains unresolved. SERFF’s mandate is deliberately narrow, designed to facilitate transmission of filings between insurers and regulators, not to manage the broader, interconnected product development and filing lifecycle. Because it primarily serves state departments of insurance, it offers little help with the internal and cross-functional workflows that dominate the filing process. And even if its new version proves more efficient for filers, it will inevitably fall behind in the fast-moving technology cycle we now inhabit.

Complicating matters, filings touch several major functions within an insurance organization. Actuarial, compliance, marketing, claims, and IT all need to know what is being filed, what the filing introduces or changes, and when those changes will take effect. During the filing process, multiple areas may also need to support regulatory activities, including preparing actuarial exhibits, drafting form changes, and responding to regulatory inquiries. Without integrated systems, these interactions are often disjointed, relying on ad hoc communication and manual tracking.

The real transformation will come from integrated, intelligent systems that combine automation, analytics, and AI. These technologies will not only eliminate manual tasks like uploading, indexing, and data entry, they will also centralize knowledge, coordinate stakeholders, assist with compliance, and preserve a continuous institutional memory from concept to approval. As insurers evolve, filings will no longer depend on a key employee’s knowledge or disconnected spreadsheets. Instead, they will flow through unified insurance state filings software platforms that are fast, highly automated, and resilient—where expertise is amplified by technology and data resides uniformly in one system rather than scattered across disparate drives (or filing cabinets).

At Perr&Knight, this vision is reflected in the development of PK1Cloud, a unified digital platform built to address precisely these challenges and lead the industry toward a smarter, more connected future.

The Inefficiency of Today’s Filing Process

Despite decades of incremental improvements, the filings process remains one of the most labor-intensive, fragmented, and risk-prone activities within the insurance industry. For many organizations, more than half of the time and effort spent on a filing has nothing to do with actuarial analysis or regulatory interpretation; it is consumed by manual mechanics such as uploading documents, indexing exhibits, entering data into SERFF, tracking correspondence, and maintaining version control. Each of these tasks creates opportunities for delay, inconsistency, or error.

Because most companies rely on a patchwork of shared folders, email threads, and spreadsheets, even simple filings can require extensive coordination to confirm which version of a document is current or whether an exhibit was approved.

This fragmentation extends beyond the filings team itself. Product managers, actuaries, compliance staff, marketing, claims, and IT all depend on accurate, timely information about what’s being filed and when. In addition, critical components of the filing process—such as reviewing state insurance codes and comparing proposed filings to competitor submissions—are still largely manual exercises. These activities are essential for compliance and competitive positioning, yet they consume significant time and are highly susceptible to human oversight. With structured data and AI, both can be automated or accelerated, allowing teams to focus on interpretation rather than repetition.

The inefficiency is compounded during regulator interaction. Preparing responses to inquiries or objections frequently requires recreating or re-collecting the same data, exhibits, and rationale because the supporting material isn’t centralized. This often includes the same time-consuming steps of verifying code requirements or researching competitor filings to justify a company’s position. Institutional knowledge about past filings, including why decisions were made, what worked, and what didn’t, often disappears when employees move on, i.e., traveling knowledge risk.

Today’s process is workable, but it’s fragile. It relies on human continuity rather than system continuity, and on institutional memory rather than data intelligence. Until that balance shifts, insurers will remain constrained by legacy workflows that limit speed, accuracy, and adaptability.

From Automation to Integration: The Next Leap

Technology, including AI, will dramatically reduce the time and effort required to create, submit, and support rate, rule, and form filings. Much of today’s filing workload can be fully automated through integrated systems and insurance state filings software.

What once required days of effort will be completed in hours, freeing actuaries, product experts, and compliance professionals to focus on higher-value work such as pricing strategies and product innovation. Intelligent systems can generate exhibits, align documentation, and produce outputs in the exact structure required by regulators, improving accuracy and consistency while reducing rework.

Fully integrated filing environments take this a step further by connecting every stage of the process—preparation, review, submission, and regulatory response—within a single system. The process becomes visible, traceable, and consistent, transforming what has historically been a fragmented, manual function into one that operates with manufacturing-like discipline and data-driven accountability.

From Silos to Systems: Coordinating Stakeholders

Every filing touches multiple teams, and each has a distinct interest in what’s being filed and when. Marketing teams need to know what is being filed and when it will go live so they can prepare producer communications and policyholder notices. Claims needs visibility into coverage changes that could affect claim-handling procedures. The IT department must know which rate tables, rules, and forms are being revised so that the rating and issuance systems can be properly programmed and tested.

In the current environment, this coordination often depends on meetings, emails, and personal follow-up, which can be a slow and error-prone process. Modern, integrated filing systems, by contrast, allow for automated notifications, integrated calendars, and dependency tracking. Each department can see precisely what stage the filing is in, what it changes, and when implementation is expected. This ensures synchronization across the organization, reduces operational risk, and shortens the cycle from regulatory approval to market launch.

By connecting stakeholders through shared data and automated communication, the organization gains operational alignment where everyone is working from the same playbook, at the same pace, toward the same deadlines.

Archival and Institutional Memory

A modern state filings system doesn’t just manage filings; it remembers them. Unlike SERFF’s static, PDF-based recordkeeping, an integrated insurance state filings software platform can archive the entire workflow: correspondence, analyses, internal notes, version histories, decision rationales, and even bureau adoptions. This is far more valuable than a simple record of what was filed. It is a dynamic record of how it was done.

Such a system creates true institutional memory, enabling teams to retrieve not just the final product but the reasoning behind it. Future filings can draw upon this archive to anticipate regulatory questions, reuse templates, and ensure consistency across states and product lines. It transforms recordkeeping into knowledge management.

Building Resilience: Eliminating Single-Point Dependency

Modern filings platforms also strengthen organizational resilience. By systematizing the process, they remove single-point dependency risk: the exposure that arises when institutional knowledge resides in a single individual or small team. Insurance state filings software replaces this vulnerability with a single source of truth that is always accessible, always current, and always auditable.

The benefits extend beyond risk mitigation. When data, exhibits, and correspondence are centrally stored and version-controlled, employees can transition between roles without disrupting operations. Knowledge no longer travels with individuals; it stays with the organization. This continuity enhances both efficiency and governance, ensuring that expertise compounds over time.

The Human Factor: Evolving Roles

As automation handles the mechanics, the human role in filings will shift toward interpretation, judgment, and oversight. Actuaries will focus less on producing exhibits and more on validating assumptions and communicating analytical insights. Compliance experts will spend less time chasing documents and more time shaping strategy. Product teams will gain more bandwidth for innovation because their filing support will be faster and more reliable.

In this model, technology doesn’t replace expertise; it amplifies it. The professionals who understand the regulatory and actuarial nuances will remain indispensable, but they will operate in an environment that enables their insights to scale.

Conclusion: The Reimagined Filing Ecosystem

The next decade will redefine how rate filings are done. The combination of automation, integration, and AI will transform the process from a collection of disconnected manual tasks into a unified, intelligent workflow. Insurers that embrace this transformation will see faster cycle times, fewer errors, greater compliance, and ultimately a sustainable competitive advantage.

For regulators, modern insurer compliance systems will yield a clearer, more data-driven view of the filings they review, enabling faster approvals and more consistent oversight. For insurers, it will mean a world where filings are not just faster—they’re smarter. Compliance will be embedded, not appended, and systems (not solely people) will safeguard important knowledge.

At Perr&Knight, this vision is already coming to life through PK1Cloud, our unified platform designed to simplify complexity across the entire product and filing lifecycle. PK1Cloud centralizes data, automates key workflows, communicates key milestones to all stakeholders, and integrates AI-driven analytics to enhance accuracy, speed, and compliance. It also connects with trusted third-party data sources for insurance code validation and competitor rate and form filings, enabling real-time benchmarking and compliance verification.

The filings process has long been viewed as a necessary administrative burden. While regulation will always remain a fundamental part of the insurance landscape, the burden it imposes can be reduced. With solutions like PK1Cloud, that reduction is not theoretical—it’s already underway. Intelligent, integrated systems are transforming filings from a back-office necessity into an efficient capability that strengthens compliance, accelerates innovation, and connects insurers and regulators in a continuous cycle of improvement.

Contact us today to learn more about how Perr&Knight’s proprietary insurance state filings software, PK1Cloud, can help your organization get a head start on the future of filings.

Listen to a podcast-style summary of this blog post

When we developed PK1Cloud Filings (formerly StateFilings.com), our goal was to solve a problem that many insurance carriers face but often accept as a necessary inefficiency: redundant data entry across filing systems. For years, state filings teams have managed information across SERFF, internal databases, and various tracking tools, often duplicating work and increasing the risk of human error. The case of one top-20 national insurance carrier demonstrates how a centralized solution can transform that status quo – cutting administrative hours in half, reducing filing errors, and increasing operational confidence.

The Compliance Challenge: Duplicative Entry and Manual Workarounds

Before implementing PK1Cloud Filings, this national carrier’s regulatory filings team was performing dual data entry for every submission – once into SERFF and again into an internal Microsoft Access database. While this setup technically fulfilled their needs, it created persistent inefficiencies:

Over 50 hours each month were spent on duplicative data entry

Data mismatches were common, introducing unnecessary compliance risks

Staff time was consumed by low-value administrative work, driving up labor costs

This isn’t a unique situation. Across the industry, insurers often rely on spreadsheets, Access databases, or custom-built systems that are disconnected from SERFF. This fragmentation not only slows down filing teams but also creates barriers to collaboration, version control, and audit transparency.

The PK1Cloud Filings Solution: One Entry, Complete Integration

This carrier transitioned to PK1Cloud Filings as a centralized system of record for all state filings activity. Rather than entering the same data twice, the filing team now inputs it once into PK1Cloud Filings, where it is automatically formatted and transmitted to SERFF. Key platform features contributed to the transformation:

Bi-directional SERFF integration that pushes and pulls content in real time

Automated task managementand role-based workflows that reduce delays and oversight risks

Configurable form libraries and templates that streamline new product and rate filings

Dashboards and notifications that replace manual tracking and disconnected communication

The results speak clearly.

Measurable Gains: Speed, Accuracy, and Cost Reduction

After adopting PK1Cloud Filings, the insurer reported a:

52% reduction in data entry time – dropping from over 100 hours to fewer than 50 hours per month

$45,000+ in annual labor cost savings – based on average hourly wages for compliance professionals

70% drop in filing errors – as a result of reduced data duplication and improved consistency

3x faster turnaround – helping the carrier respond more quickly to regulatory timelines

100% audit readiness – with complete document versioning and visibility into filing activity

These are not abstract benefits. They represent operational improvements that directly impact bottom-line efficiency and regulatory performance.

Industry Context: Why This Matters Now

State filings are becoming more complex and time sensitive. Departments of Insurance (DOIs) are scrutinizing filings more closely, often requiring detailed justifications and supplemental information. Meanwhile, insurers are under pressure to accelerate time-to-market for product changes, particularly as competitive cycles tighten.

Regulators, too, are modernizing. The NAIC has continued to evolve the SERFF platform and has pushed for more consistency in electronic submissions. However, integration challenges remain, especially for carriers that manage filings with legacy systems or siloed processes.

In this environment, operational efficiency isn’t just a convenience; it’s a strategic requirement.

Recent trends highlight the shift:

Rate modernization initiatives in several states have shortened filing windows, demanding quicker response times

Data calls and reporting obligations have become more frequent and more detailed, increasing documentation overhead

Regulatory objections have grown in complexity, requiring better documentation and internal collaboration to resolve quickly

A centralized solution like PK1Cloud Filings helps insurers keep pace with these changes by unifying processes and reducing administrative drag.

Eliminating Redundant Systems: A Broader Organizational Benefit

Beyond compliance, the carrier in this case study saw broader organizational benefits. By removing the need for an internal Access database, they eliminated the overhead of maintaining an outdated system that required IT support and periodic troubleshooting.

In many insurance organizations, regulatory teams are forced to rely on systems that are not purpose-built for state filings. PK1Cloud Filings, by contrast, is designed specifically for the insurance industry, with functionality that aligns with how regulatory teams actually work.

This alignment leads to several ongoing advantages:

Better collaboration between actuarial, product development, and legal teams

Consistent version control, so everyone sees the same data in real time

Structured workflows that make onboarding and training new team members more straightforward

Why It Matters

Compliance is too important and too resource-intensive to be slowed by duplicative data entry and outdated tools. This case study proves that it’s possible to achieve:

Reduced operational costs

Improved compliance accuracy

Faster time-to-market

Greater audit readiness

Elimination of redundant internal systems

All by centralizing and automating what was formerly a manual, high-friction process.

Take the Next Step

Whether you’re looking to streamline workflows, reduce filing errors, or improve coordination across teams, PK1Cloud Filings offers a modern solution built for the complexity of today’s insurance environment.

Visit our website to learn more or get in touch with us directly to discuss your current state filings process. We’re happy to provide tailored guidance based on your filing needs and internal systems.

Perr&Knight has published the Q3 2025 edition of State Filings Pulse, providing the latest insights into state specific filing news, approval times by state and other filing statistics.

During the last 12 months, Texas has disapproved 7% of all filings with a disposition. An additional 7% of the filings were withdrawn during this period.

Approval times in Texas have increased notably for homeowners filings, while remaining relatively steady across other lines of business. Median times to approval are summarized below:

All Lines: Increased from 39 days in 2023 to 57 days for the 12 months ending 09/30/2025

Homeowners: Increased from 70 days in 2023 to 159 days for the 12 months ending 09/30/2025

Personal Auto: Increased slightly from 67 days in 2023 to 71 days for the 12 months ending 09/30/2025

Commercial & All Other Personal: Increased from 30 days in 2023 to 52 days for the 12 months ending 09/30/2025

The Texas Department of Insurance Filings Made Easy Manual outlines common issues found in form and rate/rule filings, which includes the items below.

All Filing Types

Cloned filings: Incorrect information (TOI, Sub-TOI, Filing Type, filing description information, State Specific tab) is uploaded in the new filing which results in additional objections being sent.

Filing company name: Names must match the Certificate of Authority (COA) issued by the Department.

TOI/Sub-TOI: Incorrect for the line of insurance or information being filed.

Line of insurance: Companies must have a COA for the line.

Filing type: Incorrect filing submission. For example, submitting a policy form as an endorsement or including rate/rule pages in form filings.

Managing general agent (MGA): The name that is submitted must match the license that is issued by the Department. Also, the MGA must be appointed by the company.

Risk purchasing groups (RPG): The name of the RPG must be included in the filing. The RPG must be registered with the Department.

Reference filings: Incorrect information submitted.

Documentation: Vague or incomplete filing memorandum. Inaccurately labeled or named documents.

Form Filings

Form name: Must be complete and match the form schedule.

Form number: Must be complete and match the form schedule including the edition date, if applicable.

TDI file number or SERFF tracking number for previously approved policy form: Missing, incorrect, or incomplete.

Form usage table: Incorrect information.

Rate/Rule Filings

Missing or incomplete actuarial support for proposed changes.

Missing one or more categories of required supporting information.

Incomplete information provided on company exhibits. Although the TDI Exhibits themselves are not required, the information requested in them is required. If you use your own version of a TDI exhibit, please make sure it contains at least as much information as the corresponding TDI exhibit. Note that using the TDI exhibits assists TDI staff in reviewing your filing.

Exhibits for a relativity analysis that show an “indicated” factor but do not document the method that produced the factor.

Exhibits that show selected relativities that do not follow the indicated relativities, with no explanation given for the differences between indicated and selected. If the proposed factors are not equal to the indicated factors, the company must explain how the proposed factors are determined from the indicated factors.

The most common objection relates to waiving the 60-day deemer period for form, endorsement, and certificate of insurance filings. The option to waive the deemer date on submission of the filing is included in the State-Specific Questions section in SERFF.

Approximately 25% of form filings approved this year did not include a waiver of the deemer date at the time of initial submission. When insurers elect not to waive the deemer, the Department will request a waiver before starting its review of the filing. While some insurers comply with this request, others choose not to waive the deemer. In many cases, insurers indicate that they will waive or extend the deemer period at a future date if needed.

Form filings where the deemer was not waived had a median time to approval of 18 days, compared to 36 days for filings where the deemer was waived.

California Filing Rejection/Withdrawal Rate at Nearly 40%

Through the third quarter of 2025, insurers continue to struggle to comply with California’s rate filing requirements. Due to a combination of rejections for lack of completeness and withdrawals for other reasons, California recorded the highest combined rejection and disapproval rate in the country, nearly 40% during the second and third quarters of 2025. When combined with approval timelines exceeding nine months, California remains the most challenging state nationwide for obtaining rate filing approval.

There is reason to expect improvement in the near future. One of the primary drivers of filing rejections has been data reconciliation issues. With the release of the October 22, 2025 edition of the state’s transmittal templates, California incorporated its data reconciliation tool directly into the template, allowing insurers to identify and correct discrepancies prior to submission. The updated template also introduces a 5% threshold, requiring differences exceeding that level to be resolved or explained in the Filing Memorandum. Previously, no threshold existed, which often led the Department to question immaterial differences. This concern was raised by one of our consulting actuaries last March during a question-and-answer session with the Department at the Association of Insurance Compliance Professionals Compliance Summit in Los Angeles. We are encouraged that the Department has since implemented a formal threshold.

Looking ahead, California plans to launch the state’s new Prior Approval Rate Application (PARA) Portal in early 2026. Insurers will have the option to complete state transmittal forms though the PARA Portal, which has enhanced data reconciliation and validation tools designed to reduce errors and improve consistency across filings. The Department has begun emailing insurers with no registered PARA Portal users, requesting designation of an initial administrator to complete registration in early January. Additional details and training will be provided by the Department ahead of the PARA Portal release, tentatively scheduled for late January 2026.

Time to Approval/Disposition by State

The table below provides a detailed breakdown, by state, of the median time to approval or disposition, based on data from State Filings Pulse, for the 12-month period ending September 30, 2025.

Rate Filings1,2

Approval Time Range (Days)

Homeowners

Personal Auto

Commercial & Other Personal

0 to 303

AL, AR, AZ, ID, IL, IN, KS, KY, LA, MI, MN, MT, NC, NE, NM, OK, OR, SD, TN, UT, WI, WV, WY

AL, AR, AZ, ID, IL, IN, KS, KY, LA, MN, MS, MT, NC, NE, NM, OH, OK, OR, SD, TN, UT, WI, WV, WY

Electronic state filings are entering a new chapter. As the NAIC rolls out its SERFF modernization initiative, insurance carriers, MGAs, and compliance professionals are adapting to a new, cloud-based system. This shift will change how filings are submitted, reviewed, and reported.

But the biggest challenge isn’t insurance state filings software or the technology itself – it’s how well organizations align around it.

Readiness Starts Inside the Organization

The most successful transitions won’t be driven by systems alone. They’ll come from organizations that are organized, communicative, and confident. That means preparing your people, reviewing your processes, and confirming that your technology partners are ready to support a dual-platform environment for submitting and tracking state filings.

The ability to operate confidently across both the legacy and modernized SERFF platforms is now a requirement, not a luxury. Modernization is no longer a theoretical concept; it is moving into active implementation. Therefore, readiness must shift from planning to execution.

Filing teams need to define their responsibilities, workflows must reflect current activity, and systems must be flexible enough to connect and scale. It is not enough to prepare once and wait. Organizations must treat readiness as an ongoing capability.

What to Expect During the Transition

Even the best internal readiness plan will face external challenges as states begin utilizing the new platform at different times. This is especially important for multi-state filers. As each state adopts the new platform based upon its readiness, filers will need to manage submissions across two environments. Tracking, status visibility, and reporting will all become more complex.

Compliance and product teams that rely on aggregated dashboards, reports, and automation tools will face new configuration demands, and coordination with IT will be more important than ever.

Preparing for What’s Next

Preparation today ensures confidence tomorrow. There are six essential steps every organization can take today to strengthen readiness and prepare for what is to come:

Stay informed – Follow updates from the NAIC and your state liaisons.

Train early – Familiarize teams with new workflows, terminology, and insurance state filings software.

Map your footprint – Take inventory of the states and lines your company files in and match them to the NAIC early adopter list.

Audit your data flows – Know where filing data connects to internal systems.

Plan for coexistence – Expect a period of overlap between platforms

Engage your vendors – Confirm that partner systems, like StateFilings.com, are ready for both environments.

Managing the Transition: Options for Every Organization

Each organization will need to determine the approach to managing the SERFF transition that best fits its structure, capacity, and goals. The chart below outlines common approaches and their implications.

Every organization’s journey will look different. What matters is selecting a path that balances control, efficiency, and resource investment.

Choosing the Right Approach for Your Organization

Approach

Description

Best for

Considerations

Manual Management

Track filings separately in each SERFF system

Smaller teams or low-volume filers

High internal coordination required; prone to human error

Internal API Integration

Build internal tools to connect directly to both SERFF systems

Carriers with strong IT resources

Requires significant upfront investment and ongoing maintenance

Centralized Filing Desk

Designate internal team to manage all filings across systems

Organizations with multiple product lines

Needs clear ownership and training; benefits from process consistency

Managed Services

Outsource filing management to an experienced partner

Organizations looking to reduce internal workload

Relies on vendor expertise; requires strong communication

Vendor Platform

Use a system like StateFilings.com for unified filing and reporting

Carriers seeking automation, accuracy, and visibility

Offers scalable support, centralized tracking, and minimized IT effort

How StateFilings.com Bridges the Gap

Among these options, StateFilings.com from Perr&Knight stands out for its ability to unify both legacy and modernized SERFF environments into a single, seamless environment. This all-in-one insurance state filings software connects to both platforms, consolidates all filing activity and correspondence, and maintains a complete audit trail across systems. Centralization like this reduces manual work and improves visibility across jurisdictions.

Real-time filing data gives compliance and product teams instant and comprehensive insights without the need for data reassembly. Filing information flows smoothly into existing reporting tools and dashboards, while the system’s cloud-based architecture minimizes IT maintenance. As new states and lines of business transition, StateFilings.com scales right alongside them, ensuring your systems and processes stay aligned with regulatory change.

With the proper preparation and the right tools, modernization becomes more than a compliance requirement: it becomes an opportunity to improve efficiency, reduce risk, and strengthen outcomes. If your organization is preparing for SERFF modernization, now is the time to act.

For insurance carriers, program administrators, MGAs, and the like, the accuracy of policy administration systems (“PAS”) is crucial, not only for profitability and policyholder retention, but also for compliance. Every form, notice, and rate/premium that leaves a PAS must align with what was filed with the Department of Insurance (“DOI”).

Regulatory scrutiny doesn’t end when a filing is approved. Through market conduct exams, regulators also scrutinize whether what was issued and charged matches the forms, rates and rules that were filed. The NAIC Market Regulation Handbook outlines standards insurance companies must adhere to, including: “All forms, including policies, contracts, riders, amendments, endorsement forms and certificates are filed with the insurance department…” and “The rates charged for the policy coverage are in accordance with filed rates…”.

This provides examiners with a clear playbook to follow during a market conduct exam: compare issued forms and rates to approved filings. Here’s what our insurance compliance consulting experts want you to know about taking a proactive approach to market conduct exams.

Why Testing Matters

Discrepancies between approved and utilized materials are among the most frequent findings our insurance consulting team has seen in market conduct exams. Common pitfalls include:

Policies rated with unfiled factors or outdated tables

Use of non-approved consent or disclosure forms

Notices missing state-mandated language

When there is a gap between what is filed and issued, the consequences can be substantial, including policyholder restitution, interest, fines, mandated remediation, and reputational damage. The good news is: a disciplined program of regular testing closes the gap, facilitates compliance, and readies you for all types of market conduct activity.

Exempt From Filing Does Not Mean “Off The Hook”

Some lines of business are exempt from form and/or rate/rule filing requirements in certain states. That doesn’t mean state-specific coverage requirements don’t apply. Rather, it simply means the materials do not need to be filed with the DOI before they are issued. Insurers still carry the burden of making sure their materials comply with state requirements and they are still subject to regulatory scrutiny in the form of a market conduct exam.

When filing exemptions apply, rather than comparing issued forms and rates to approved filings, examiners will compare them to state insurance laws and regulations during the market conduct examination. If discrepancies are found, companies may still be subject to consequences.

How To Structure Regular Testing

Building a sustainable, repeatable testing program isn’t rocket science. In fact, during our decades of insurance consulting, our product design experts have identified these five key components that are essential to any testing program:

Baseline library Maintain a centralized location that retains all filed forms, rates and rules, with version control, for comparison.

Scenario-based testing Run end-to-end transactions (quote → bind → issue → bill → renew → cancel) on a sample of risks to capture all system outputs.

Premium calculation check Recalculate premiums for a cross-section of risks using filed rate manuals, and reconcile them to what was charged, reconciling to the penny.

Form generation and content validation Confirm the system attaches the correct forms, applies approved variability, and inserts all required disclosures.

Regular cadence Perform regular testing, prioritized based on risk factors that may include: high-volume products, active DOIs, known previous issues, product updates (e.g., recent filing activity).

Benefits of Proactive Testing

The benefits of proactive testing far outweigh the time and expense. In addition to preventing costly exam findings, proactive testing provides the following additional benefits:

Demonstrates disciplined compliance control and a strong governance framework that regulators respect

Improves speed-to-market by reducing last-minute compliance fixes and re-filing delays

Strengthens collaboration between compliance, actuarial, and IT teams, ensuring aligned implementation

Provides executive leadershipwith confidence that compliance risk is proactively managed

Builds trust with regulators and policyholders by showing transparency and consistency

Protects brand reputation through accurate, compliant policy issuance at every stage of the product lifecycle

How Testing Supports Statistical Data Reporting

Accurate PAS workflows and outputs do more than just ensure filed-to-issued compliance. They are also the foundation of statistical data reporting compliance with regulators and statistical agents. Regular testing helps:

Premium & exposure accuracy

Confirm that premiums generated align with risk classifications, coverages and filed rates for each policy transaction to prevent misreporting of earned/written premium and exposures.

Form and rating component reporting

Ensure the data within policy forms and rating component details are accurately captured and flow downstream to the statistical reporting sources and reports.

Policy and claims linking

Validate that claim and policy data are linked at the policy, risk classification and coverage level and can be traced back to filed policy statistical data, supporting actuarial reviews of statistical submissions.

Regulator trust

Reduce the risk of DOI inquiries, costly resubmissions and data quality penalties, or corrective action associated with inaccurate data capture.

By integrating output testing with data reporting, insurers create a closed loop: filed forms and rates drive system output, which in turn drives compliant statistical submissions.

Insurance Consulting Experts Can Help

Partnering with credentialed, experienced insurance compliance consulting professionals like Perr&Knight can help you get ahead of any market conduct exams your company might face. Our product design experts have experience with regulatory requirements in all jurisdictions and can provide guidance and support to help design or evaluate your testing program.

Contact the team at Perr&Knight today to discuss your policy administration testing.

Perr&Knight has published the Q2 2025 edition of State Filings Pulse, providing the latest insights into state specific filing news, approval times by state and other filing statistics.

During the last 12 months, New York has disapproved 12% of all filings with a disposition. This has been a fairly consistent ratio from 2023 to 2025. The time to approval has been increasing in the state for rate filings as follows:

All Lines: 58 days in 2023 to 120 days for 12-months ending 06/30/2025

Homeowners: 62 days in 2023 to 233 days for 12-months ending 06/30/2025

Personal Auto: 90 days in 2023 to 157 days for 12-months ending 06/30/2025

Commercial & All Other Personal: 38 days in 2023 to 88 days for 12-months ending 06/30/2025

Below are the top five objections, which were gathered by our consulting actuary experts and product design consultants reviewing publicly available filings over the last 12 months.

Issues with Rate Filing Sequence Checklist Items:

Exhibit RT-2 (Policyholder Rate Level Changes): Missing histogram including a step-by-step derivation of the RT-2 histogram data.

Exhibit RT-1 (Side-by-Side Comparison): Missing side-by-side comparison. Red-lined manual pages do not satisfy this requirement.

Exhibit JDG-1 (Explanation of Key Areas of Judgment): Insufficient or no support for judgment.

Clarification on whether a form is mandatory or optional, and objecting that optional forms with coverage effects must have an associated rate reduction to avoid unfair discrimination.

Side-by-side comparison for new forms based on or similar to a form that was previously approved by this Department.

Failure to outline all the proposed changes in the explanatory memo.

Not including State Tracking Numbers for referenced competitors, Rating Service Organization Adoptions or prior filings, when applicable.

According to our consulting actuary experts, it is fairly common for filings to not be fully compliant with the New York Rate Filing Sequence Checklist instructions. They recommend reviewing this before each filing and establishing templates with all the required information to ensure compliance.

California Filing Rejection Rate Skyrockets

As mentioned with the release of Q1 2025 edition of State Filings Pulse, the rejection rate for rate filings in California has jumped since the implementation of the Complete Rate Application (CRA) regulation in October 2024 (CCR §2648.4). Below is the latest update.

2024: 3%

Q1 2025: 14%

Q2 2025: 30%

One of the main reasons filings are rejected is due to data reconciliation issues. Insurers should be performing all the data checks in California’s Prior Approval Rate Application – Data Quality and Reconciliation Checklist. If the Company has reasons for any data reconciliation differences, these should be explained in the filing. To help insurers comply, the Department has developed a Prior Approval Rate Application (PARA) Portal and Data Reconciliation Tool. The beta version is currently being tested by participating insurers.

If you are one of the insurers having issues with filings being rejected in California, Perr&Knight’s actuarial experts can review filings prepared by insurers and recommend changes needed to comply with the state’s requirements. This includes running the data through Perr&Knight’s proprietary data reconciliation tool.

Time to Approval/Disposition by State

The table below provides a detailed breakdown, by state, of the median time to approval or disposition, based on data from State Filings Pulse, for the 12-month period ending June 30, 2025.

Excluding Rate Filings1,2

Approval Time Range (Days)

Homeowners

Personal Auto

Commercial & Other Personal

0–303

AL, AR, AZ, ID, IL, IN, KS, KY, LA, MI, MN, MT, NC, NE, NM, OK, OR, SD, UT, WI, WV, WY

AL, AR, AZ, ID, IL, IN, KS, KY, LA, MN, MS, MT, NC, NE, NM, OK, OR, SD, TN, UT, WI, WV, WY

Benjamin Franklin once stated, “An ounce of prevention is worth a pound of cure.” This is certainly the case when submitting an insurance filing to a State Department of Insurance (“DOI”). Preparing a meticulous and comprehensive submission can help mitigate issues, but it doesn’t necessarily eliminate the possibility of objections from the DOI.

Objections arise for various reasons, including but not limited to regulatory changes, interpretation differences, and jurisdictional nuances. When the dreaded form or rate interrogatory is received, here are some best practices from our experienced insurance filing support teams.

Don’t panic

Despite your best efforts to submit a complete, comprehensive filing, it is always possible that you will receive objections from one or more DOIs. The more lines of business you write and the more jurisdictions you operate in, the more likely you are to receive an interrogatory. Each DOI has specific filing and supporting documentation requirements – some with commonalities. Accepting objection letters and responding promptly are simply processes that enable you to move quickly, adjust the filing, and move closer to approval.

Read carefully and respond thoroughly

If an objection is not answered correctly, it will delay the filing’s approval. Thoroughly read each objection and only answer the question asked. Each objection should be responded to professionally, clearly, and concisely. The response should be complete and provide adequate supporting documentation, but without providing extraneous answers that may not be relevant to the respective objection. Submit your response for peer review or return to it with fresh eyes to confirm all the above have been addressed.

Make it easy for the reviewer

Provide necessary documentation in a manner that is easy for the regulator to address each interrogatory sufficiently. Logically rename file attachments and reference file names within the responses, where applicable.

If you revised a form, rating, or other piece of supporting documentation based on an objection, make a clear note in your response (e.g., “XYZ document has been revised and is attached [see FILE NAME] and replaces the first version of the same document.”)

In short, make it straightforward for the reviewer to follow the changes from the initial submission to the objection to the revision.

Reach out

Statute interpretations vary by jurisdiction, so a lack of understanding of why you did not fulfill a regulatory requirement does not necessarily indicate a shortcoming on your part. Not only are some statutes interpreted differently across regions, but the wording is sometimes vague.

If your objection letter contains an item you don’t understand, do not be afraid to contact the DOI directly, either through email, phone, or video call. Discussing the objection via video call has benefits, especially if you have received the same objection multiple times. Putting a face to a name and connecting personally with a person at the DOI can help you quickly clarify what you need to correct so the approval process doesn’t stall.

Track dates meticulously

Responding to the objection(s) by the date provided by the regulator is important. Response(s) not received by the due date could result in additional delays in the filing (e.g., disapproval). However, if you believe you will require more time than the state allows, submit an extension request as early as possible to give the reviewer time to assess and issue a revised due date. Note that some states have limitations on when extensions must be requested and how many extensions may be allowed.

Keep files and correspondence organized

Before submitting the responses and supporting documentation, ensure all documents are organized and correctly attached. Always double-check responses for accuracy and completeness, making sure you have read all pages of the objection letter (a common mistake is failing to see and respond to questions on subsequent pages). It is also important to submit the information as requested by the regulator (e.g., as part of the response, SERFF Supporting Documentation).

Leverage technology to stay organized. Tracking software like StateFilings.com was explicitly developed to align with the insurance state filings process, enabling users to store and track submissions, due dates, correspondence, and supporting documents in a central, secure repository. Two-way integration with SERFF allows users to post filings to each state, receive communications directly from DOIs, and track due dates – all in one place.

Stay professional

Responding to objections might cause frustration, but always reply to interrogatories with a cooperative attitude. Don’t take the objection personally. At the end of the day, the regulator is just doing their job. In any communication, written or verbal, treat the regulator with respect. Remember, regulators share your objective of arriving at an approved submission. Using a kind tone demonstrates professionalism, which opens the door for further communication.

Research

It can help to review previouslyapproved filings and search for responses to similar objections. If you use an example of a previously approved filing, be prepared, as the filing may have been approved in error. While a level playing field among companies is important, each filing must be looked at on a case-by-case basis. If the previously approved filing language is a clear-cut violation of a statute, administrative rule, or commissioner’s order, the DOI may respond that it will ask the approved company to file and correct the approval error.

Rely on experts

Managing multiple filings across all jurisdictions is a logistical challenge for insurance companies at every scale. Partnering with actuarial consulting and insurance filing support teams like the experts at Perr&Knight can save time, clear up questions, and accelerate speed-to-market. Our industry veterans possess decades of experience submitting filings in all 51 U.S. jurisdictions across all lines of business. Leveraging this expertise can help streamline your filings. We can provide guidance at any stage of the state filings process, including support for objections to filings we did not initially submit. We’re here to help at any point in the process – even under tight deadlines.

It’s crucial to anticipate potential areas of concern and address them proactively to minimize delays and ensure a smooth approval process. When responding to the DOI’s objections, especially the “tough” interrogatories, it is essential to be thorough, clear, and prompt. By following these strategies, you can effectively respond to filing interrogatories and enhance the likelihood of a favorable outcome.